By Ryan McMaken

Money-supply growth fell year over year again in March, but March’s decline was the smallest money-supply drop recorded in 16 months. Moreover, the money supply in March grew—month over month—by the highest rate in two years. The current trend in money-supply growth suggests a continued turnaround from more than a year of historically large contractions in the money supply. As of March, the money supply appears to be in a period of stabilization. The money supply is still flat or down on a year-over-year (YOY) basis, but there has been clear growth over the past several months.

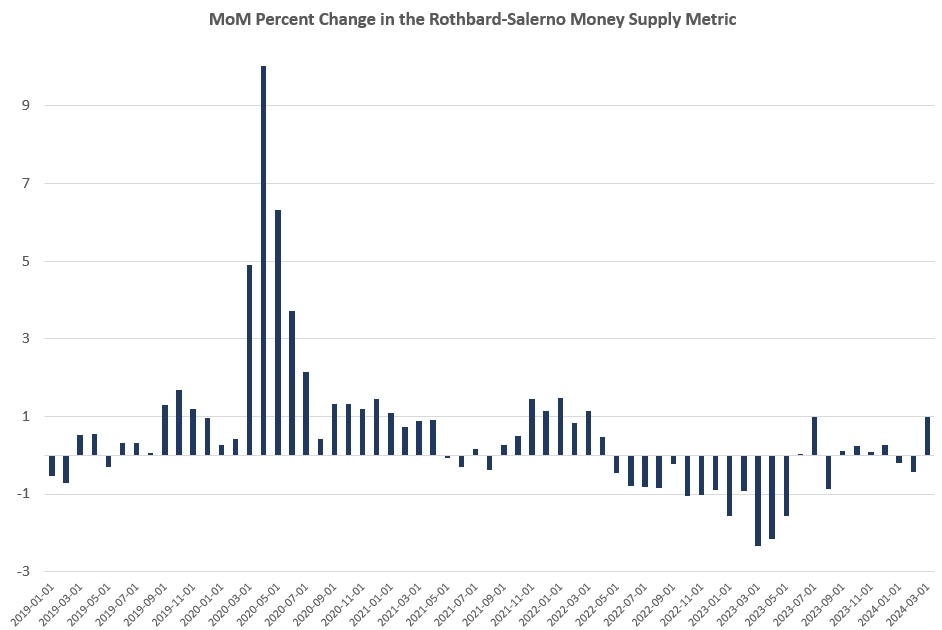

Money-supply growth has now been negative—year over year—for 17 months in a row. During March 2024, the downturn continued as YOY growth in the money supply was at negative 2.57 percent. That was up from February’s rate of decline, which was negative 5.76 percent, and was a much smaller rate of decline than that of March 2023, which had a rate of negative 9.87 percent. With negative growth now lasting more than a year and coming in below negative 5 percent for most of the past year and a half, money-supply contraction is the largest we’ve seen since the Great Depression. Before 2023, at no other point for at least 60 years had the money supply fallen by more than 6 percent YOY in any month.

Those dramatic drops in the money supply appear to be over for the time being. Indeed, when we look at month-to-month changes in the money supply, we find that the money supply increased by 0.98 percent from February to March. That’s the largest growth rate since March 2022. In month-to-month measures, money supply growth has been positive during seven of the past 10 months, further suggesting that the new trend in money supply is either flat or returning to sustained upward growth.

The money supply metric used here—the “true,” or Rothbard-Salerno, money supply measure (TMS)—is the metric developed by Murray Rothbard and Joseph Salerno and is designed to provide a better measure of money supply fluctuations than M2. (The Mises Institute now offers regular updates on this metric and its growth.)

In recent months, M2 growth rates have followed a similar course to that of TMS growth rates, although TMS has fallen faster than M2 in the YOY measures. In March, the M2 growth rate was negative 0.28 percent. That’s up from February’s growth rate of negative 1.82 percent. March 2024’s growth rate was also up from March 2023’s rate of negative 3.74 percent. Moreover, M2 also shows more overall growth than TMS, with M2 increasing by 1.1 percent from February to March this year.

Money supply growth can often be a helpful measure of economic activity and an indicator of coming recessions. During periods of economic boom, money supply tends to grow quickly as commercial banks make more loans. Recessions, on the other hand, tend to be preceded by slowing rates of money supply growth.

It should be noted that the money supply does not need to actually contract to signal a recession. As shown by Ludwig von Mises, recessions are often preceded by a mere slowing in money supply growth. But the drop into negative territory we’ve seen in recent months does help illustrate just how far and how rapidly money supply growth has fallen. That is generally a red flag for economic growth and employment.

All that said, recessions tend not to become apparent until after the money supply has begun to accelerate again after a period of slowing. This was the case in the early 1990s recession, the Dot-com Bust of 2001, and the Great Recession.

In spite of last year’s sizable drops in total money supply, the trend in money supply remains well above what existed during the 20-year period from 1989 to 2009. To return to this trend, the money supply would have to drop another $3 trillion or so—or 15 percent—down to a total below $15 trillion. Moreover, as of March, the total money supply was still up by more than 30 percent (or about $4.5 trillion) from January 2020.

The TMS money supply is now up by more than 185 percent from 2009. (M2 has grown by 145 percent in that period.) Out of the current money supply of $19 trillion, $4.6 trillion—or 24 percent—of that has been created since January 2020. Since 2009, more than $12 trillion of the current money supply has been created. In other words, nearly two-thirds of the total existing money supply has been created just in the past 13 years.

With these kinds of totals, a 10 percent drop in the money supply only puts a small dent in the huge edifice of newly created money. The U.S. economy still faces a very large monetary overhang from the past several years, and this is partly why after 17 months of negative money-supply growth, we have only seen a slowdown in employment for the past several months. (For example, full-time job growth has turned negative while the total number of employed workers has been flat since late 2023.) Moreover, consumer price index (CPI) inflation remains well over the 2 percent target rate, and mainstream economists’ predictions of significant “disinflation” have been wrong.

The Fed and the Federal Government Need Lower Interest Rates

The Federal Reserve, like most central banks, is motivated by two conflicting political challenges. The first is price inflation. Regimes fear high levels of price inflation because high inflation is known to lead to political instability. One way that central banks fight price inflation is by allowing interest rates to rise.

The second challenge is found in the fact that a regime’s central bank is expected to help the regime issue debt and engage in deficit spending. Central banks’ main tool in offering this help involves keeping interest rates on government debt low. How do central banks do this? By buying up the government’s debt, thus artificially boosting demand for the government’s debt and pushing interest rates back down. The problem is that buying up government debt usually involves creating new money, thus putting upward pressure on price inflation.

So, in times of rising price inflation, central banks face two contradictory tasks: keeping price inflation low while also keeping interest rates low.

This is where the Federal Reserve is right now. In spite of the fact that the predicted “disinflation” has not materialized—and CPI inflation is not headed back to 2 percent—the Fed in recent weeks has made it clear it has no plans to raise its target policy interest rate. Politically speaking, the Fed can’t let interest rates rise because the Fed is expected to prevent any significant increases in interest paid—i.e., yields— on government debt.

Recently, Daniel Lacalle explained some of the details of the problem:

“The decision of the Fed [to not further tighten the money supply] comes when the global demand for Treasuries is under question. Foreign holdings of Treasuries have risen to an all-time high, but the figure is misleading. Demand has weakened relative to the supply of new bonds. In fact, an expected surge in new issuances by the Treasury creates a headache for the Federal Reserve. Borrowing will be significantly more expensive when public debt interest payments have reached $1 trillion, and investor demand remains robust but not enough to keep pace with an out-of-control deficit.

“China’s holdings of U.S. Treasury bonds have fallen for two consecutive months to $775 billion, according to the U.S. Department of the Treasury, and Japan’s weak yen may need a Bank of Japan intervention to sell U.S. reserves, which means disposing of Treasury bonds.”

Given all this, it’s rather surprising that money-supply growth did not turn positive sooner than it did.

What the Fed is doing now is probably best described as a “wait and hope” strategy. The Fed is refusing to allow interest rates to rise, but it isn’t lowering the target rate either. Rather, it appears the Fed is holding the target rate steady just hoping that something will happen to bring Treasury yields back down that doesn’t require the Fed to print more money to buy more Treasurys and risk a new, politically damaging surge in price inflation. “Hoping” is not much of a strategy, however, and the likely outcome is that the Fed will err on the side of keeping interest rates low so the regime can borrow more money. This will mean more price inflation for ordinary people.

Discover more from USNN World News

Subscribe to get the latest posts sent to your email.