By Kevin Stocklin

It has been a year since a string of U.S. regional bank failures, together with the collapse of global heavyweight Credit Suisse, caused many to fear that a major financial crisis was imminent.

But, by the summer of 2023, the panicked withdrawals by frightened depositors largely subsided.

In February, however, New York Community Bank (NYCB) appeared to resurrect the crisis when it announced $2.4 billion in losses, fired its CEO, and faced credit downgrades from rating agencies Fitch and Moodys.

In what has become a familiar tale for U.S. regional banks, NYCB’s share price plummeted by 60 percent virtually overnight, erasing billions of dollars from its market value, and its depositors fled en masse.

“I think that there’s more to come,” Peter Earle, a securities analyst and senior research fellow at the American Institute for Economic Research, told The Epoch Times.

Underlying this year’s turbulence is the fact that many regional banks are sitting on large portfolios of distressed commercial real estate (CRE) loans. according to Mr. Earle. And many are attempting to cope through a process called “extend and pretend,” in which they grant insolvent borrowers more time to pay in hopes that things will get better.

“There is trouble out there, and most of it probably won’t be realized because of the ability to roll some of these loans forward and buy a few more years, and maybe things will recover by then,” he said.

“But all it does is it kicks the can down the road, and it basically means a more fragile financial system in the medium term.”

NYCB’s problem was an overwhelming exposure to New York landlords who were struggling to stay solvent. At the start of this year, the bank had on its books more than $18 billion in loans to multifamily, rent-controlled housing developments.

This situation was particularly concerning given that NYCB had been the safe-haven institution that rescued Signature Bank, another failing regional bank, in March 2023.

Much of what took down banks such as Signature Bank in last year’s banking crisis was an unmanageable level of deposits from high net worth and corporate clients that were too large to be insured by the Federal Deposit Insurance Corporation (FDIC).

People walk by the First Republic Bank headquarters in San Francisco on March 13, 2023. (Justin Sullivan/Getty Images)

In Signature Bank’s case, about 90 percent of its deposits were uninsured, and depositors rushed to withdraw their money when the bank came under stress from losses in the cryptocurrency market.

Another source of stress for regional banks was their inability to cope with an aggressive series of interest rate hikes by the Federal Reserve to combat inflation. Many banks that held large bond portfolios yielding low fixed rates found that the value of these portfolios declined sharply, creating unrealized losses.

While these portfolios, often made up of U.S. Treasury securities, were considered safe from a credit perspective, they were subject to market risk, and their loss of value sparked concerns about the banks’ solvency in the event they had to be sold. As stock traders rushed to sell the shares of banks with large exposures to interest rate risk, customers became spooked and raced to withdraw their money.

Consequently, unrealized losses quickly became actual losses as banks were forced to sell bonds and loans at a loss in an increasingly futile attempt to make panicking depositors whole.

Rate Hikes Cease, Problems Remain

Today, while interest rates remain high, they are relatively stable. And yet concerns about the health of U.S. regional banks remain because of their large exposure through CRE, including office buildings, multifamily housing units, and retail spaces.

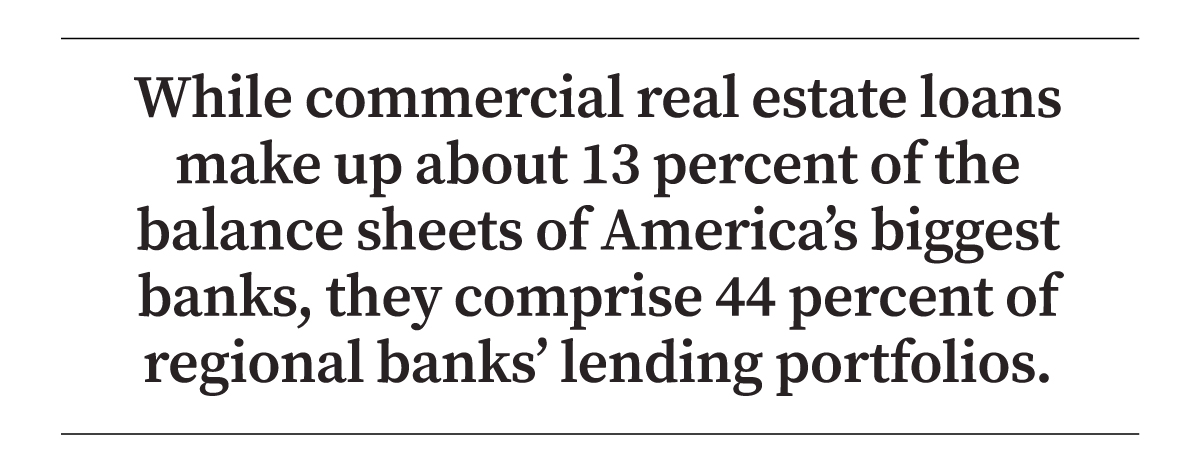

While CRE loans make up about 13 percent of the balance sheets of the biggest U.S. banks, they make up 44 percent of regional banks’ lending portfolios. CRE loans designated as nonperforming doubled as a percentage of U.S. banks’ portfolios from 0.4 percent in 2022 to 0.81 percent by the end of 2023.

In total, there are about 130 regional banks in the United States, with a little more than $3 trillion in assets. These banks, which each have between $10 billion and $100 billion in assets, are typically more exposed to the boom and bust of local markets but also to specific sectors within those markets where they have been able to operate profitably.

While other credit sectors, such as home mortgages, car loans, and corporate loans, are generally the domain of larger financial institutions, regional banks have found a profitable niche in lending to real estate investors. But in the past several years, commercial landlords have been taking hits from two directions.

Since the introduction of lockdowns and the rise of work-at-home culture during the COVID-19 pandemic, many corporations have viewed office rents as a cost ripe for cutting.

According to an April CRE report by Commercial Edge, the office vacancy rate across the United States was 18.2 percent as of March, an increase of 1.5 percent over the prior year.

“U.S. office vacancy rates have increased in recent years as companies embrace remote and hybrid work and re-examine their office footprints,” the report reads. “The increases are not concentrated in just one market or sector.”

Buildings in lower Manhattan, New York City, on April 16, 2021. Since the introduction of lockdowns and the rise of work-at-home culture during the COVID-19 pandemic, many corporations have viewed office rents as a cost ripe for cutting. (Spencer Platt/Getty Images)

The report states that the demand for office space among both tech and financial companies has dipped sharply in places such as San Francisco, Seattle, Dallas, Charlotte, and Boston. As employees opt—or demand—to work from home, companies increasingly avoid spending money on empty offices.

A February report by TD Bank found that across the United States, remote workdays have risen from 5 percent to 7 percent of total workdays before the COVID-19 pandemic to 30 percent over the past two years.

Consequently, the value of many office properties can be a fraction of what they were when loans were originally issued. This means that lending criteria, such as loan-to-property-value ratios, are significantly worse, leaving banks the option of reducing the loan size or taking a lower-quality asset into their books.

Many CRE loans, which typically have maturities of between five and 10 years, are now coming due and must be refinanced at higher interest rates.

Nearly $1 Trillion in Loans Coming Due

According to the Mortgage Bankers Association, $929 billion in commercial mortgages will come due this year, making up 20 percent of the $4.7 trillion in total outstanding CRE loans.

TD Bank estimates that another $535 billion is set to mature in 2025.

For commercial landlords, this means that their financing costs will rise exponentially, even as their rental income shrinks. This impairs debt service ratios, and for their lenders, it indicates that new loans are much more risky.

Other issues facing retailers include the escalating cost of what is known as “retail shrink,” or losses from shoplifting and damage to inventories.

“Once simply considered a cost of doing business, retail shrinkage resulted in profit losses exceeding a staggering $100 billion in 2022,” reads a February report by Ernst & Young, an accounting and consulting firm.

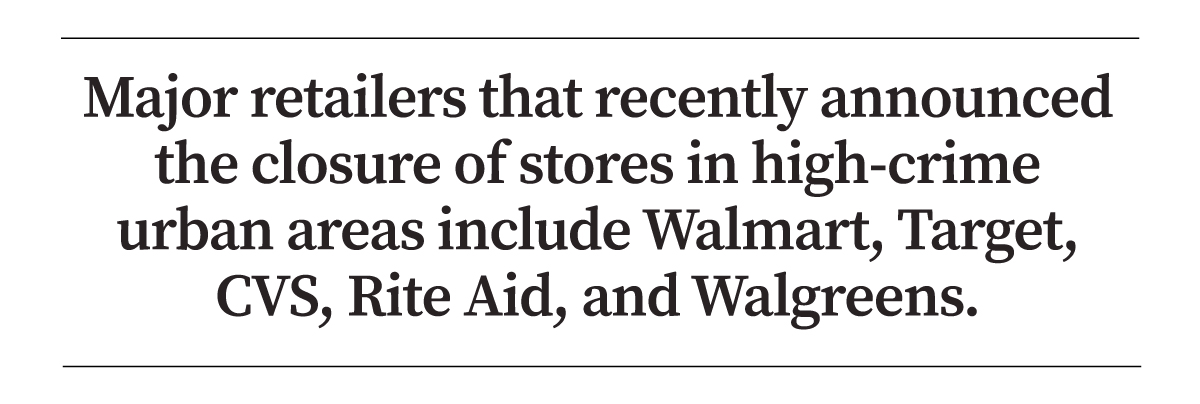

Major retailers that have recently announced the closure of stores in high-crime urban areas include Walmart, Target, CVS, Rite Aid, and Walgreens.

An official statement from Target in September 2023 declared that it “cannot continue operating these stores because theft and organized retail crime are threatening the safety of its team and guests, and contributing to unsustainable business performance.”

A cyclist rides by a Target store that is slated for closure in Oakland, Calif., on Sept. 29, 2023. (Justin Sullivan/Getty Images)

Regulators at the Fed and the FDIC say they are monitoring the loan situation and that disaster is not imminent. They are reportedly working behind the scenes with banks to resolve outstanding problems in their loan portfolios.

“We have identified the banks that have high commercial real estate concentrations, particularly office and retail and other ones that have been affected a lot,” Fed Chairman Jerome Powell told the Senate Banking Committee in March.

“This is a problem that we’ll be working on for years more, I’m sure. There will be bank failures, but not the big banks.”

Buying Time

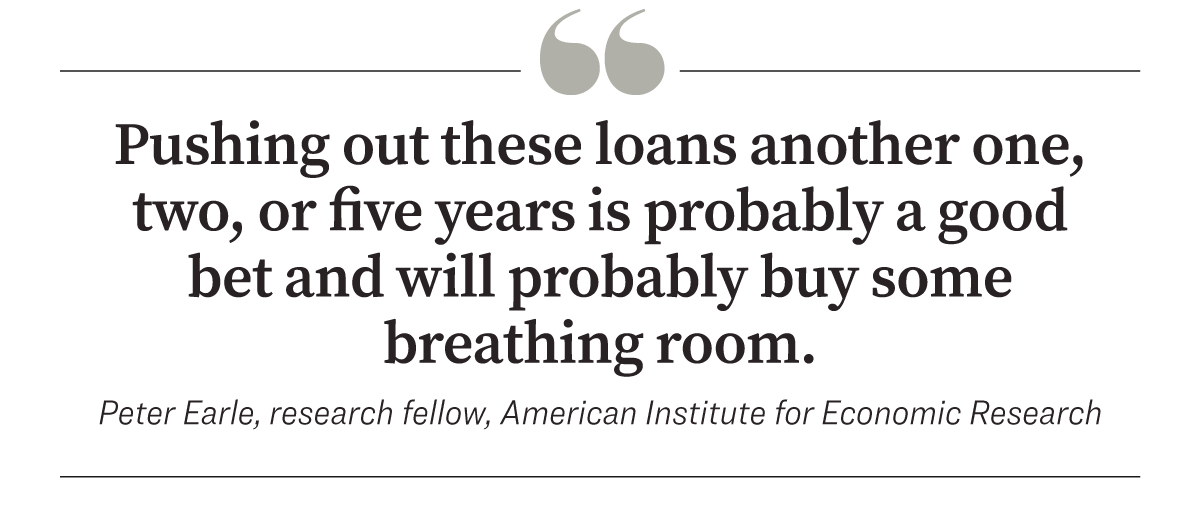

Mr. Earle said he sees inflation gradually coming under control and the prospects for a “soft landing” and lower interest rates improving.

“I think the Fed is going to lower rates pretty much no matter what,” he said. “And for that reason, pushing out these loans another one, two, or five years is probably a good bet and will probably buy some breathing room.”

Part of the solution may be to rezone some of the properties, for example from malls or office buildings to residential spaces or assisted living facilities, so that they can become more profitable down the road, according to Mr. Earle.

In the interim, many regional banks are looking to downsize their CRE loan portfolios, but that often requires selling them at a significant loss in a buyers’ market. Ultimately, those losses will significantly reduce their capital base, requiring them to recapitalize either by selling more equity or being acquired by a larger bank.

Standard and Poor’s regional bank index is up by nearly 30 percent from a year ago, indicating some optimism about a recovery for smaller U.S. banks. But the index remains well below its high at the start of 2022.

Until the CRE market recovers, however, it is not clear where regional banks can go to restore profitability. They will need to make a credible case that they can find a way to become profitable again in order to attract the investors that they will need to rebuild their capital base.

Discover more from USNN World News

Subscribe to get the latest posts sent to your email.