By Law Ka-chung

Central banks have signaled in this “super week” their intentions to end the tightening cycle soon. But they dare not to confirm anything because inflation is unwilling to ease while recession is unwilling to arrive. Both of these recent symptoms conclude that the tightening effect has not been enough. There are two possibilities here: Either the tightening is enough while it takes time to be effective, or the total tightening so far is not enough where inflation will not revert to target even observing for a dozen months ahead.

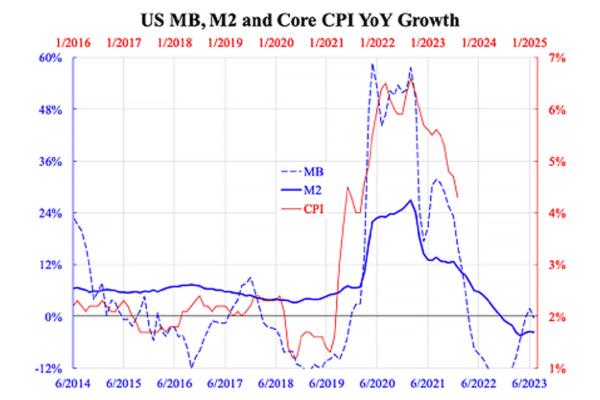

Which is the reality? Central banks themselves don’t know, and that is why they decide, meeting by meeting. The accompanying chart shows the relationship between the monetary base (MB), M2, and core consumer price index (CPI), all in year-over-year (YoY) growth rates and for this round of inflation only (within the past decade). The time gap between the two horizontal axes suggests monetary policy takes roughly 1.5 years to be effective. As tightening was most aggressive in Q2-3 last year, inflation should cool down quickly in the upcoming two quarters.

This probably explains why the Federal Reserve tends now to take the wait-and-see approach. However, quite many inflation indicators do not point to a sharp fall direction. Core services inflation is now stuck near 3 percent, while wage inflation has remained above 4 percent for a year. Core inflation in other areas like the Eurozone is not falling satisfactorily, while that in the UK and Japan are even flat (not falling). Worst of all, energy prices have been reflating recently, further fuelling inflation. Remember, all central banks take overall but not core inflation as targets.

As central banks claim that recession can be avoided, this is a strong signal to the market that they are prepared to do more. But the possibility of a recession could overturn everything. Historical experience suggests that a recession is usually not known until it happens. This means central banks will be forced to keep tightening as recession is not there where inflation is high. But they will also be forced to cut quickly and likely aggressively once recession begins. Isn’t it unlikely, anyway? That is what central banks claim, yet the yield curves completely disagree.

Returning to the accompanying chart, the core inflation trend roughly follows those of narrow and broad money (MB and M2, respectively) but is not so on track. If the red line were on blue, then core inflation should now be 3 percent rather than over 4 percent. This is yet another symptom suggesting tightening might not be enough. In the face of a potential recession that drags everything down with huge force, inflation will come down accordingly. But the underdoing of tightening could generate more serious inflation in the next round when recession fades out.

Inflation is more like a long-term health problem, while recession is like an imminent short-term sickness. People tend to care more about short-term issues than long-term (like focusing more on weather than on climate). Nevertheless, as the long-term issue gets serious enough, the damage is permanent.

Discover more from USNN World News

Subscribe to get the latest posts sent to your email.