By J.G. Collins

January jobs printed at 353,000 new jobs, according to the Establishment Survey from the Bureau of Labor Statistics (BLS), a collection of job creation data from businesses. November and December jobs creation revisions added another 126,000 new jobs. The number far surpassed the consensus estimate of 187,000 new jobs.

The BLS’s Household Survey, which calculates the number of people taking jobs, and is viewed as eliminating workers taking more than one job, showed 31,000 fewer people working in December than in January. Notably, according to the Household Survey, full-time employment declined by 63,000 while part-time employment increased by 96,000.

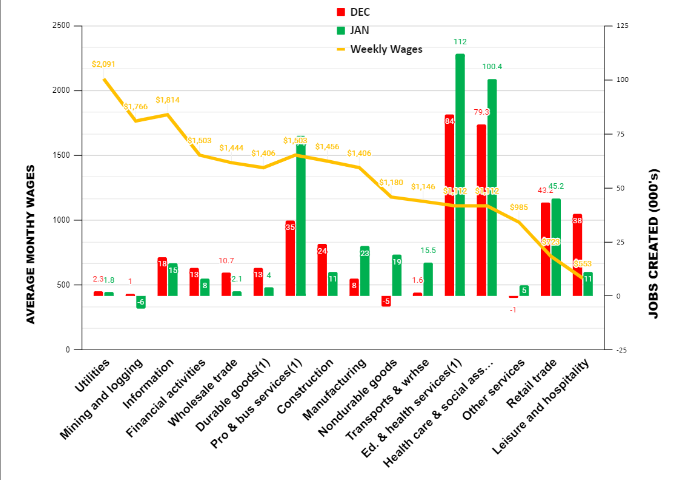

Let’s look at our exclusive schedule of jobs creation by average weekly wages:

Once again, the largest gains in employment in January were in education and health services, with 112,000 new jobs, which includes 100,400 healthcare and social assistance jobs. These sectors are largely supported by government spending, a trend we have seen for several months. The next largest new job creation sector was in professional and business services, a routine pattern early in the year as companies and firms ramp up hiring for year-end financial and tax reporting.

Opinion and Analysis

It’s important to remember that there’s a lot of “noise” in this report, as there are all January jobs reports, due to seasonality and population adjustments that are beyond the scope of this opinion piece. Suffice it to say, the jobs report is good, but will be revised next month.

As with last month’s better-than-expected jobs numbers, today’s jobs report should disabuse investors who held sanguine notions that a Federal Reserve rate cut will come in the first half of the year. Moreover, if the Phillips curve still holds sway, we are definitely not “done” with inflation, as we have written elsewhere. We still hold to the notion that the Federal Reserve’s overnight rate is going to be in the range of 6 percent in order to cool inflation and bring it down to the Fed’s 2 percent target, assuming they still hold to that rate, as Fed Chair Jerome Powell has asserted, but about which we’re circumspect, especially given an election year. (After all, William Dudley, former chair of the Federal Reserve Bank of New York, told his former colleagues in 2019 they should do everything they can to defeat then-President Donald Trump in the 2020 election.)

We think the Fed should have boosted rates at its last two meetings, a point we made in our December jobs report. Not only would it have helped trim inflation but also it would have given the Fed more latitude to cut rates if the economy goes into recession, as we think is still likely.

We believe that the Fed has been more restrained in its rate increases than it would otherwise be largely because of the adverse effect interest rates have had on the banking sector, particularly middle-market and small banks. That sector has seen the value of their reserves—typically held in bonds—sharply erode as rates escalated from near zero up past 5 percent. (Bond values move inversely with interest rates.)

We believe those reserves—and the U.S. economy—will face a critical turning point as office leases that commenced before the pandemic start to expire and are abandoned by companies that allow workers to work from home. That will lead to defaults by borrowers and that will adversely affect bank liquidity ratios. We expect this to become an increasing and cascading issue in the year ahead, perhaps even leading to a banking crisis toward the end of the year.

There is also a chance, albeit small, that the continued congressional disregard for the national debt and deficit, and the ongoing de-dollarization of the global economy, will cause the Fed to lose control of rates to a circumspect global market.

Absent some gray swan—which seems increasingly less gray and more white—such as the Middle East blowing up into an expanded war more deeply involving the United States, or an acceleration of the aforementioned real estate value collapse, we estimate first-quarter 2024 to print in around 2.25 percent, plus or minus a quarter of a percent.

Other Data Points in January

The Institute for Supply Management’s Manufactuer’s Purchasing Managers Index (PMI) for January showed the industrial economy is contracting more slowly than last month, and improving, somewhat, by 2 percentage points at 49.1 (A reading below 50 signals contraction.) It is the 14th consecutive month of contraction.

On the other hand, the ISM Services Index for December (the latest available) showed the service economy expanding, but more slowly, at 50.6 versus 52.7 in November.

The Job Openings and Labor Turnover Survey (JOLTS) for December, released on Jan. 30, declined, with 31,000 fewer jobs openings in December than in November. Total separations decreased by 36,000.

Privately owned housing units authorized by building permits in December were at a seasonally adjusted annual rate of 1,495,000. This is 1.9 percent above the revised November rate of 1,467,000 and is 6.1 percent above the December 2022 rate of 1,409,000.

For December, personal income and outlays, released on Dec. 26, showed disposable personal income up 0.3 percent in current dollars and 0.1 percent in chained 2017 dollars. (“Chained dollars” is a measure of inflation that takes into account changes in consumer behavior in response to changes in prices.) Personal income in current dollars was also up 0.3 percent.

The December Personal Consumption Expenditures (PCE) price index from a year ago, excluding food and energy, released the same day, and reported to be the Federal Reserve’s preferred measure of inflation, printed at 2.9 percent. PCE inflation, also called “headline inflation,” remained unchanged at 2.6 percent.

The RCM/TIPP Economic Optimism Index (previously the IBD/TIPP Economic Optimism Index) fell 10.1 percent in December, to 40.0. Half of the survey’s respondents believe we are already in a recession, according to TIPP CEO and pollster Raghavan Mayur.

Discover more from USNN World News

Subscribe to get the latest posts sent to your email.