By Kevin Stocklin

As Wall Street banks take an increasingly optimistic view of America’s economy, several traditional indicators are sending signals that all is not well.

And as the Fed inches closer to achieving its single-minded goal of taming inflation, it appears to have become hesitant, uncertain what its next steps should be.

Signals from market data are mixed, and some economists say the Fed is looking in all the wrong place for answers.

First, the good news.

This week, Goldman Sachs chief economist Jan Hatzius stated that “we have further reduced our 12-month US recession probability back to 15% from 20% in July … This change reflects continued encouraging inflation news, a favorable real income outlook, and the decline in the jobs-workers gap.”

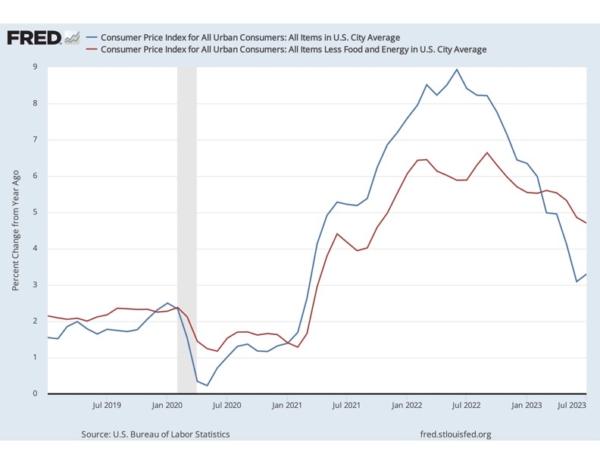

The Federal Reserve’s campaign of interest rate hikes has thus far succeeded in driving inflation within sight of its 2 percent target, and the fact that wage increases appear to have exceeded inflation for the first time under the Biden administration bodes well for consumer spending, which comprises approximately two-thirds of America’s GDP.

Advertisement – Story continues below

Labor markets, where demand for workers had sharply exceeded supply, appear to be shifting back in employers’ favor, with some workers who had previously dropped out now returning to work.

In addition, the housing market appears to be cooling as well. During a period in which buyers fled cities and enjoyed record-low mortgage rates, average home sale prices skyrocketed from about $375,000 in 2020 to about $550,000 in 2022. As mortgage rates have doubled since, house prices have fallen back to around $500,000 today.

All of this suggests that the Fed’s campaign of hiking interest rates to tame inflation will likely hit a pause or even reverse. For this reason, many analysts are envisioning a “soft landing,” in which inflation is tamed without a major recession.

Behind these trends, however, a number of key signals are flashing red.

‘Sleepwalking into a Recession’

“We are sleepwalking into a recession because the Fed has excessively squeezed the money supply,” Steve Hanke, professor of economics at Johns Hopkins University and former member of President Reagan’s Council of Economic Advisors, told The Epoch Times.

“The money supply, measured by M2, is contracting at an unprecedented -3.7 percent per year,” he said. “The Fed’s tight squeeze means that a recession will make landfall in 2024.”

The M2 measure of America’s money supply, currently about $21 trillion, refers to all of the cash Americans have on hand, plus the money deposited in checking accounts, savings accounts, and other short-term investments such as certificates of deposit (CDs).

Generally, increasing the money supply faster than an economy’s ability to increase production will lead to inflation while increasing the money supply at a slower rate will constrain growth and increase unemployment.

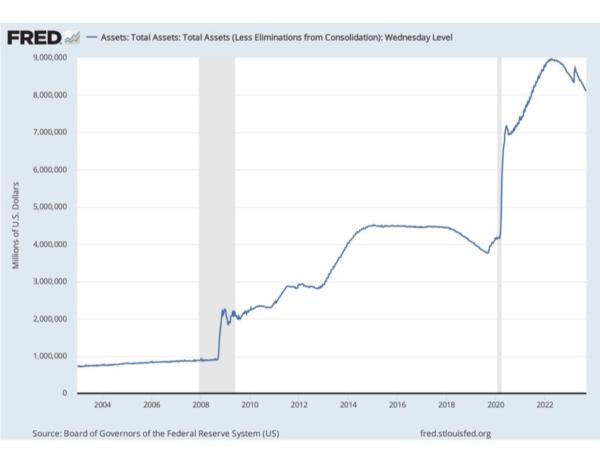

According to a Reuters report, however, America’s money supply is now shrinking at the fastest rate since the 1930s. This is due to several factors, including the Fed reducing its balance sheet through a process called “quantitative tightening,” a mass withdrawal of bank deposits, and a more restrictive environment for bank lending.

In an effort to spur growth after the 2008 mortgage crisis and the 2020 pandemic lockdowns, the Fed bought bonds by the trillions, flooding the markets with cash, and expanded its holdings from $900 billion to $4 trillion in 2008. Starting in 2020, it more than doubled its holdings to $9 trillion by 2022.

As part of its inflation-fighting efforts over the past year, the Fed has been gradually reducing its balance sheet down to the current level of about $8.24 trillion.

“The problem now is the reverse of the problem that they’ve had for the last couple of years,” Thomas Hogan, senior research faculty at the American Institute for Economic Research and former chief economist for the U.S. Senate Banking Committee, told The Epoch Times.

“For the last two years, they ignored price stability in order to avoid a recession, at a major cost to the economy and to Americans,” he said.

Inflation was the highest rate in 40 years, he said, adding that it has reduced Americans’ real incomes by more than 20 percent since the pandemic.

Bloated Balance Sheet

“Normally, the Fed can kind of play with the money supply a little bit to keep the size of the money supply proportionate to the size of the economy,” Richard Stern, Director of the Heritage Foundation’s Center for the Federal Budget, told The Epoch Times.

But since 2008, the Fed has been aggressively expanding it well beyond growth rates, taking on the role of chief problem solver for America’s economy.

The sheer size of the Fed’s balance sheet today has made it the dominant player in money markets and amplified the effects of its actions, as evidenced by the failure of several regional banks as a result of the Fed’s actions to raise interest rates.

But with its currently bloated balance sheet and its recent history of printing trillions of dollars, the Fed appears to have painted itself into a corner.

“As the Fed is looking at it, they have two choices: If they don’t print money, interest rates skyrocket,” Mr. Stern said. “In fact, the move from 3 percent prime lending rates and 3 percent mortgage rates to 7 percent mortgage rates and 8.5 percent prime lending rates, started the day the Fed announced they weren’t going to print more money.

“So if they don’t print money, the federal government just steals all the oxygen out of the room; it starves every business, and interest rates go to the moon,” Mr. Stern said. “If they do print money, then inflation goes to the moon.”

The Case for a Recession

The voice of doom among Wall Street analysts was Deutsche Bank. In a report released this week titled “The Case for a Recession,” Deutsche Bank pointed to indicators such as the inverted yield curve, banks’ increasing unwillingness to lend, consumers’ depleted savings, a deteriorating labor market, and rising delinquency rates on credit cards and auto loans—all of which set the bank’s “recession probability” at greater than 90 percent over the next 12 months.

Deutsche Bank, however, conceded that “soft landing prospects have improved” in recent months, noting that their calculation of recession probability has now come down from nearly 100 percent. The bank attributed this sliver of optimism to moderating inflation, the resolution of supply chain issues that had choked production during the pandemic, a possible bottoming-out in home construction, and a rebound in retail sales.

All things considered, however, the bank concluded that pulling off a soft landing “will be tough.”

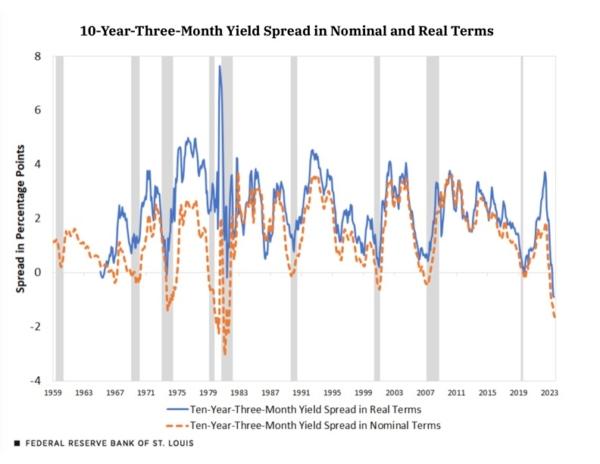

Other indicators flashing red include the yield curve, which tracks interest rates for bonds according to their maturity dates. Under normal circumstances, interest rates are lower for short-term than for long-term bonds, given that risk increases the farther out in time one extends.

An inverted yield curve, where long-term rates are below short-term rates, often indicates a coming recession. Currently, the yield curve is strongly inverted, at about the same degree as 1928, just prior to the Great Depression.

In addition, the American consumer is looking financially less healthy with each passing month. Personal savings rates are falling steadily, and debt levels are rising, leading many analysts to fear that defaults will soon follow.

A report by the San Francisco Fed, stated that, of the $2.1 trillion in aggregate cash savings Americans accumulated during the pandemic from government handouts and other sources, only about $190 billion was left as of June of this year. Looking ahead, the report states, “there is considerable uncertainty in the outlook, but we estimate that these excess savings are likely to be depleted during the third quarter of 2023.”

Consumers Running Out of Cash

As consumers run out of cash, it will become increasingly difficult for consumption to drive GDP growth. To add to this, companies are starting to slow hiring and lay off workers.

For all its optimism, Goldman Sachs announced this week that it would cull between one and five percent of its workforce or between 400 and 2,000 jobs. This comes in the wake of a January cut of about 3,200, or 6.5 percent of Goldman’s workforce, following a decline in profits at the investment bank and losses at the consumer bank.

This is in line with other financial firms like Morgan Stanley, which cut 3,000 jobs in the second quarter of this year, and Barclays and Charles Schwab, which both announced this week that significant layoffs were coming. The financial sector is following the tech sector, which so far this year has laid off approximately 240,000 staff.

Approximately 1,000 tech companies have laid off workers in the past year, including Amazon (27,000 workers), Meta/Facebook (21,000), Google (12,000) and Microsoft (10,000).

The spike in interest rates is also taking its toll on housing, which, for many Americans is their single most valuable asset. With mortgage rates more than doubling since 2021, many buyers are finding that they cannot afford monthly mortgage payments, and many sellers are unable to put their homes on the market if that means exiting their existing mortgage, which could be at a rate of 3 percent or lower, to take on a new mortgage at twice the cost.

In addition, there is the fear of looming defaults in the commercial real estate sector, as employees continue to avoid going into the office and companies avoid having employees. This has caused companies to cancel or downsize leases on commercial spaces, creating severe problems for many landlords, who are also faced with the prospect of rolling over real estate loans at higher rates at a time of lower profitability.

The largest holders of commercial real estate loans are regional banks, raising concerns that another chapter in the regional bank crisis may be about to begin. And this could have a snowball effect of further tightening loan markets and reducing the money supply even further.

Speaking to the degree of uncertainty about next steps, Fed Chairman Jerome Powell stated in a speech on Aug. 25 that the Fed was “navigating by the stars under cloudy skies.” However, some analysts believe the Fed is looking in entirely the wrong direction.

“The key data it focuses on centers around what is happening in the labor market and with inflation,” Mr. Hanke said. “Both of these happen to be very lagging indicators.

“In short, the Fed is looking at noise,” he said, “It is totally ignoring the only relevant signal available,” which is the sharp contraction of the money supply.

“This is why I conclude that the Fed is, in fact, flying blind—ignoring the signal and only paying attention to the noise,” he said.

Discover more from USNN World News

Subscribe to get the latest posts sent to your email.